The article below is an excerpt from a recent edition of Bitcoin Magazine PRO, Bitcoin Magazine’s premium markets newsletter. To be among the first to receive these insights and other on-chain bitcoin market analysis straight to your inbox, subscribe now.

Bitcoin volatility returns with an exchange rate crash.

Aug. 17, marked the return of the much-awaited and notorious bitcoin volatility. After several months of consolidating around the $30,000 level with historically low realized and implied volatility in the bitcoin market, the price finally awakened, bringing about the biggest liquidation event bitcoin has seen in years. Contrary to some opinions by reporters and analysts, the bitcoin crash was not triggered by rumors of SpaceX selling bitcoin or any other news-based event. Unlike a stock, bitcoin doesn’t have earnings calls or bad news about future prospects that can tank the price or dampen the network’s fundamentals.

Yes, events such as the approval (or dismissal) of a spot bitcoin ETF could change the market’s expected flows, but this was not the case during Thursday’s price crash. Instead, the market move was a good, old-fashioned derivative liquidation, a simple instance of more sellers than buyers, with the resolution being a price-clearing mechanism to the downside.

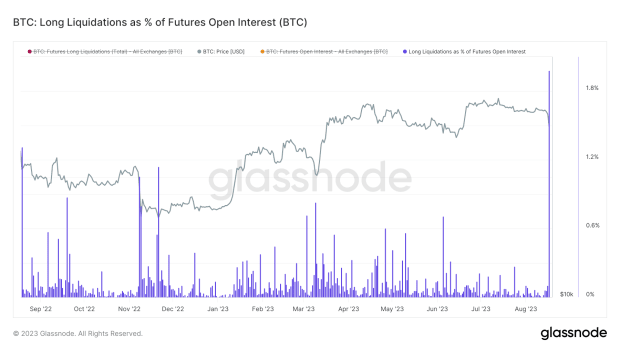

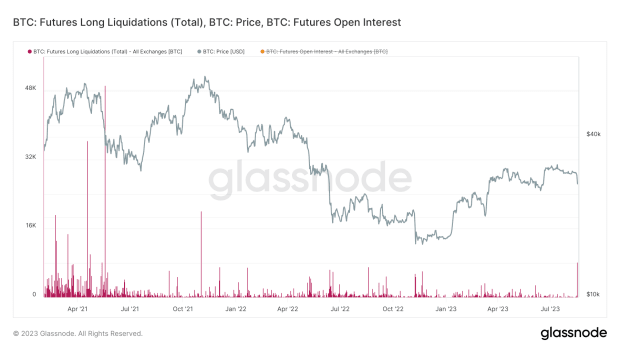

Nearly 2% of longs were liquidated in the extreme price move.

In previous issues, we wrote about bitcoin’s historically low realized and implied volatility, noting that such periods lead to large bounces in volatility and explosive breakouts in either direction. Obviously, the recent resolution was to the downside, but it could lead to a new regime in bitcoin, at least temporarily, as the market attempts to find a new equilibrium in the short-to-intermediate-term.

Since this was largely a derivative phenomenon, let’s explore some of the mechanics behind this massive move. In bitcoin, while the options market is less developed and mature compared to equities, there has been growth relative to the futures market in recent years, and growth in both markets compared to the spot market since 2017. It’s important to note that the proliferation of a futures/derivatives market isn’t necessarily good or bad. With an equal amount of long and short positions, the net impact over a long enough time frame is neutral. However, in the shorter-to-medium term, a developing derivatives market on top of the spot market can lead to large dislocations that result in unexpected volatility, with the market trading aggressively in one direction or the other to resolve the imbalance.

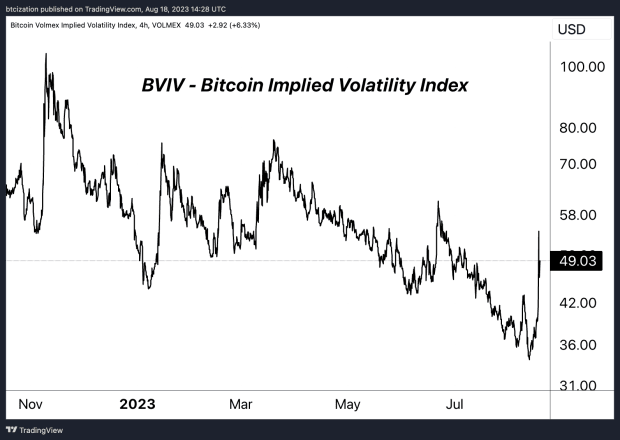

The explosive price correction brought about an equally violent rise in volatility.

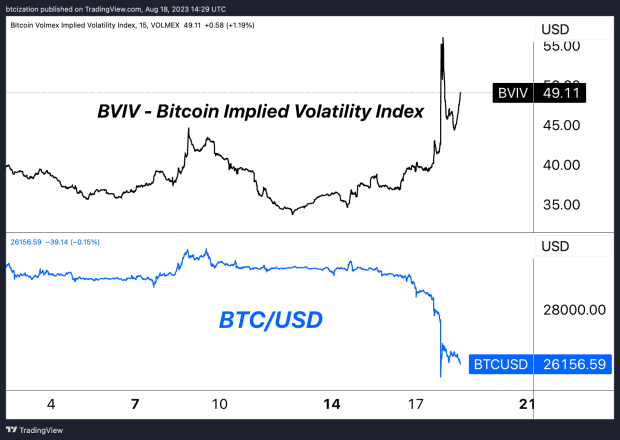

When observing a period of downtrending implied volatility derived from pricing in the options market, we can see what traders and speculators think an asset’s future volatility will look like. Short volatility strategies, whether simple or complex, are essentially bets on lower and/or stagnant volatility in the future. In this case, observing the trend in bitcoin’s implied volatility through the Volmex Bitcoin Implied Volatility Index (BVIV), we can conclude that selling or shorting volatility became a popular trade over the summer months, effectively restricting the bitcoin market to a given price range.

When market participants sell volatility through options, market makers respond by adjusting their hedges in the underlying asset, creating a stabilizing “pinning” effect near certain price levels where there is substantial open interest. To maintain a neutral position, market makers dynamically buy or sell the underlying asset in response to price movements of options, reinforcing the pinning effect. This equilibrium, however, can be shattered by unexpected events or shifts in sentiment, causing market makers to rapidly re-hedge. This leads to a sudden and significant price and volatility movement, reflecting the delicate and interconnected nature of options trading, market making and asset dynamics. This is precisely what occurred.

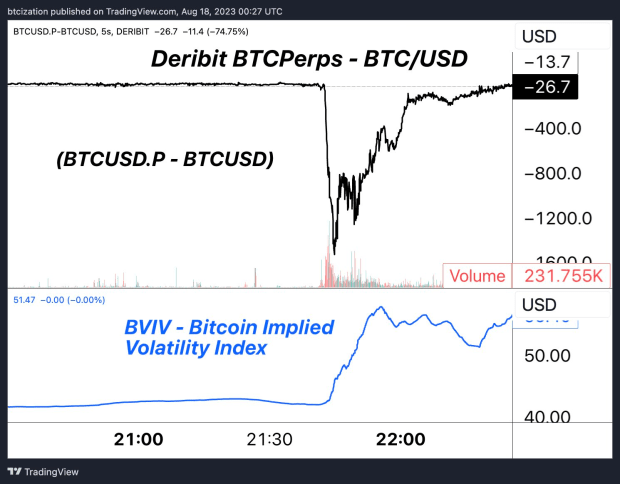

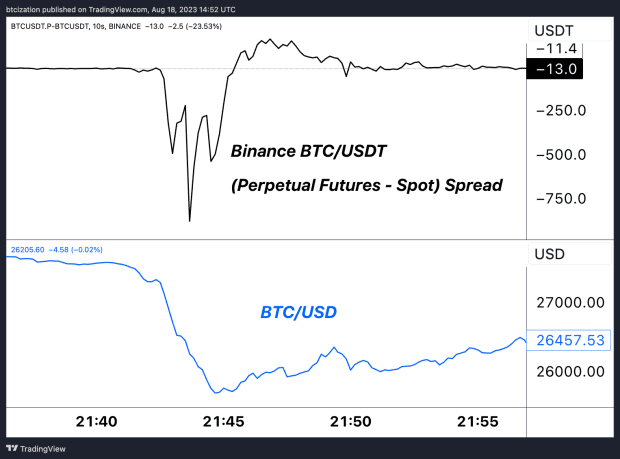

Looking at Deribit, the primary options marketplace for bitcoin/crypto, the spread between their perpetual swaps market and the spot bitcoin market widened massively as implied volatility expanded. Participants who had been making money by shorting or selling volatility were caught unexpectedly, leading to a massive dislocation and liquidation event.

As implied volatility expanded, the spread between perpetual swaps market and spot bitcoin widened on Deribit.

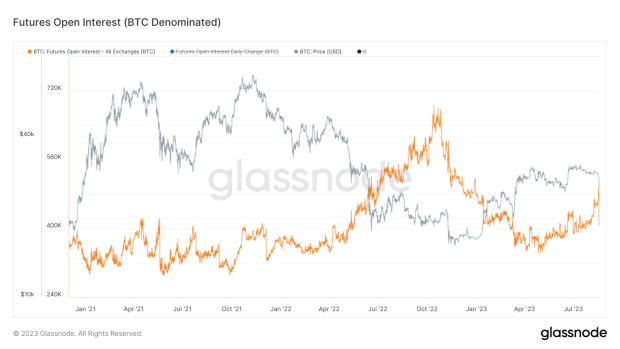

All that being said, this wasn’t just an options-driven event. There was growing leverage in the futures market as well. Spot market volumes at multi-year lows combined with growing derivative volumes and open interest in addition to volatility near multi-year lows, was akin to lighting a match near a pile of dynamite and waiting for ignition. Alas, a spark was lit.

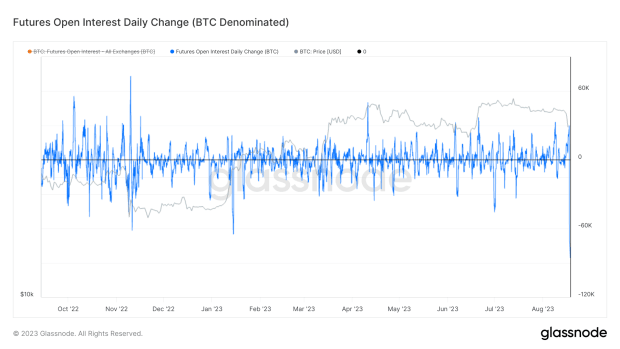

In bitcoin-denominated terms, the daily change in open interest was larger than the collapse of FTX, with 89,000 BTC less open interest than 24 hours prior.

After the move, there was 89,000 bitcoin less open interest than 24 hours prior.

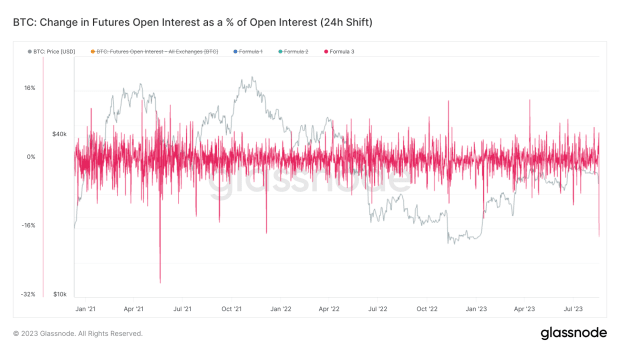

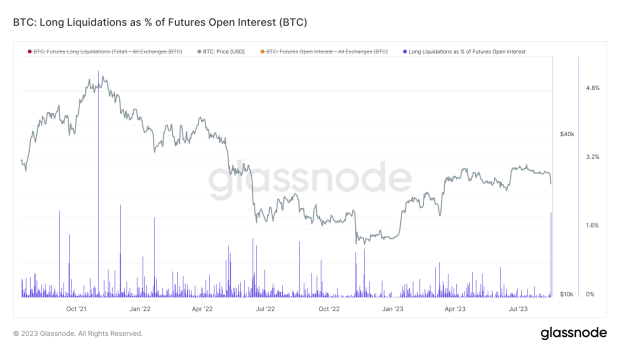

As a percentage of the futures market, with a 24-hour period to match up the timelines, the move was equivalent to 18% getting wiped out or closing, something that hasn’t been seen since December 2021.

The clearing of 18% of open interest hasn’t been seen since December 2021.A build up of open interest led to a clearing event on Thursday.A build up of open interest led to a clearing event on Thursday.

Looking only at open interest liquidations, Glassnode finds 8,141 BTC getting liquidated during Thursday’s move, the largest since November 2021, and approximately 2% of open interest that forcefully got liquidated or margin called.

8,141 bitcoin were liquidated during Thursday’s move.Long liquidations spiked during the price correction.

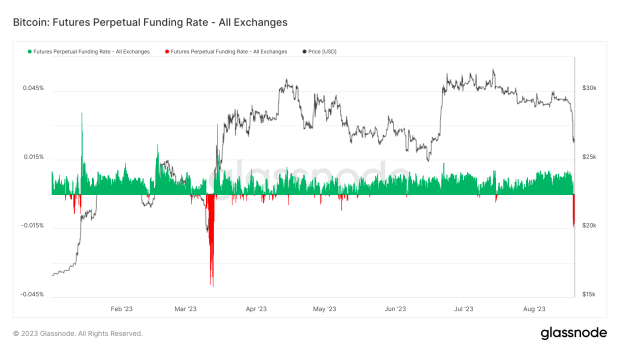

Taking a look at funding rates — the variable interest rate paid between long and short positions in the perpetual futures market to incentivize traders to keep the contract price close to the spot market — funding fell to its lowest level since the March banking crisis when Silicon Valley Bank failed and USDC depegged. This shows just how large the dislocation in the derivatives market was relative to the spot market. While it’s too early to draw conclusions about a significant short bias in the market due to the negative funding rate, we will monitor the market over the coming days and weeks. A period of sustained negative funding with rising open interest could bring about conditions conducive to a short squeeze, although this has yet to develop.

A period of sustained negative funding with rising open interest could bring about conditions conducive to a short squeeze.On Binance, the spread between perpetual swaps market and spot bitcoin widened as the price crashed.

Final Note:

In conclusion, while Thursday’s move was the largest bout of volatility seen all year and the largest bitcoin derivative-driven phenomenon in quite some time, it is typical of periods of extremely low realized and implied volatility in any market, let alone that of a notoriously volatile and unpredictable digital asset still in its monetization phase. In the short term, we now expect a pickup in volatility and greater uncertainty as the price tries to find a new equilibrium point, with plenty of news ahead regarding potential bitcoin spot ETF approvals heading into 2024.

That concludes the excerpt from a recent edition of Bitcoin Magazine PRO. Subscribe now to receive PRO articles directly in your inbox.

History has demonstrated that when regulators attempt to intrude on liberties, individuals find workarounds.In recent days and weeks, U.S. Treasury Secretary Janet Yellen has been raising the alarm about what she perceives to be a rising “misuse” of cryptocurrencies, which she argues are used mainly “for illicit financing” by unsavory groups. During her confirmation hearing,…

BRD, one of the most secure cryptocurrency mobile wallets, trusted by over 2 million users in 170 countries, now enables Canadian customers to purchase bitcoin, ether and bitcoin cash for some of the lowest fees in the industry. Through its partnership with the fast-growing Canadian crypto trading platform Coinberry, BRD’s Canadian customers will be able…

In the past, infrastructure deals have represented new industrial opportunities for America, and now should be no different.“Infrastructure” is defined as the basic physical and organizational structures and facilities (e.g. buildings, roads, power supplies) needed for the operation of a society or enterprise.There have been instances in our country’s history where infrastructure projects/legislation have been…

CommerceBlock is releasing Mercury Layer today, an improved version of their variation of a statechain. You can read a longer form explanation of how their Mercury statechains work here. The upgrade to Mercury Layer represents a massive improvement against the initial statechain implementation, however unlike the initial Mercury Wallet release, this is not packaged as

In a world of destruction and creation, Bitcoin is the work of Daedalus, a representation of everything just, useful and beautiful.Throughout the whole of history many means of exchange have disappeared. Supposing that money as we know it today, were to also disappear? The world would not miss it for a single day, for its…

This is an opinion editorial by Michael Matulef, an independent student of Austrian economics and member of the Mises Institute.The impending U.S. presidential election has ignited a spark of excitement within the Bitcoin community, as various prospects have begun to vocalize their support for Bitcoin. Rising political interest in Bitcoin has culminated in the emergence…

Bitcoin Has Become The Main Focus For The Digital Assets Division Of Fidelity Investments.Bitcoin has become the main focus for the digital assets division of Fidelity Investments. In an interview with the Boston Globe, Christine Sandler, head of sales and marketing for Fidelity, said that 90 percent of Fidelity’s biggest clients were asking about Bitcoin.…

ANC Pharmacy is enabling bitcoin payments via Binance Pay at more than 1,000 locations across Ukraine.One of the largest pharmacy chains in Ukraine, ANC Pharmacy, has partnered with Binance to enable bitcoin and cryptocurrency payments at all of their locations. With over 1,000 stores across the country, it is one of the largest implementations of…

Bitcoin is the free market alternative to inept economists using their not-so-invisible hands to manipulate various economies across the globe.This is an opinion editorial by Max Borders, a well-published author and a contributor for Bitcoin Magazine.Well into the Great Recession, arch-Keynesian Paul Krugman wrote that what drew him to economics was, “The beauty of pushing…