The article below is an excerpt from a recent edition of Bitcoin Magazine PRO, Bitcoin Magazine’s premium markets newsletter. To be among the first to receive these insights and other on-chain bitcoin market analysis straight to your inbox, subscribe now.

Bitcoin volatility returns with an exchange rate crash.

Aug. 17, marked the return of the much-awaited and notorious bitcoin volatility. After several months of consolidating around the $30,000 level with historically low realized and implied volatility in the bitcoin market, the price finally awakened, bringing about the biggest liquidation event bitcoin has seen in years. Contrary to some opinions by reporters and analysts, the bitcoin crash was not triggered by rumors of SpaceX selling bitcoin or any other news-based event. Unlike a stock, bitcoin doesn’t have earnings calls or bad news about future prospects that can tank the price or dampen the network’s fundamentals.

Yes, events such as the approval (or dismissal) of a spot bitcoin ETF could change the market’s expected flows, but this was not the case during Thursday’s price crash. Instead, the market move was a good, old-fashioned derivative liquidation, a simple instance of more sellers than buyers, with the resolution being a price-clearing mechanism to the downside.

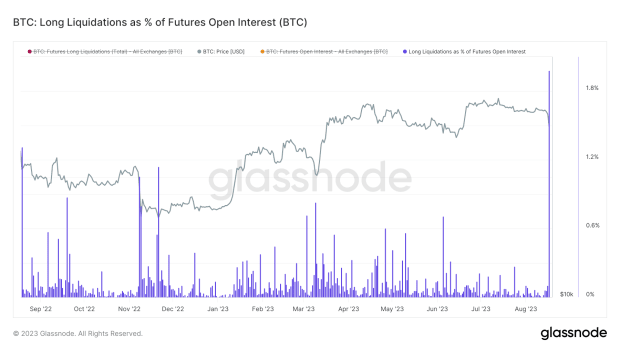

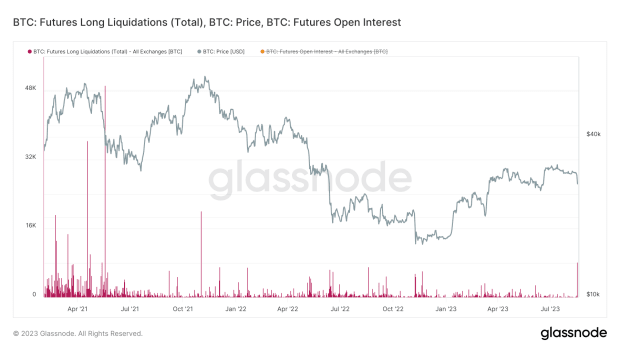

Nearly 2% of longs were liquidated in the extreme price move.

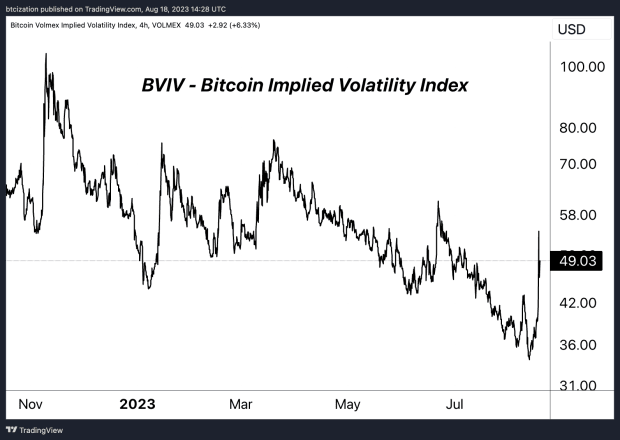

In previous issues, we wrote about bitcoin’s historically low realized and implied volatility, noting that such periods lead to large bounces in volatility and explosive breakouts in either direction. Obviously, the recent resolution was to the downside, but it could lead to a new regime in bitcoin, at least temporarily, as the market attempts to find a new equilibrium in the short-to-intermediate-term.

Since this was largely a derivative phenomenon, let’s explore some of the mechanics behind this massive move. In bitcoin, while the options market is less developed and mature compared to equities, there has been growth relative to the futures market in recent years, and growth in both markets compared to the spot market since 2017. It’s important to note that the proliferation of a futures/derivatives market isn’t necessarily good or bad. With an equal amount of long and short positions, the net impact over a long enough time frame is neutral. However, in the shorter-to-medium term, a developing derivatives market on top of the spot market can lead to large dislocations that result in unexpected volatility, with the market trading aggressively in one direction or the other to resolve the imbalance.

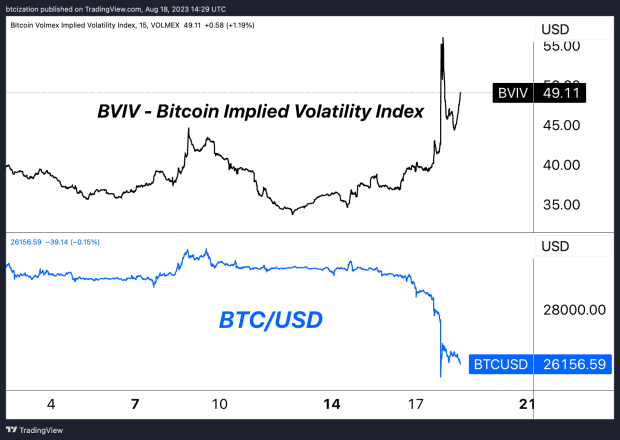

The explosive price correction brought about an equally violent rise in volatility.

When observing a period of downtrending implied volatility derived from pricing in the options market, we can see what traders and speculators think an asset’s future volatility will look like. Short volatility strategies, whether simple or complex, are essentially bets on lower and/or stagnant volatility in the future. In this case, observing the trend in bitcoin’s implied volatility through the Volmex Bitcoin Implied Volatility Index (BVIV), we can conclude that selling or shorting volatility became a popular trade over the summer months, effectively restricting the bitcoin market to a given price range.

When market participants sell volatility through options, market makers respond by adjusting their hedges in the underlying asset, creating a stabilizing “pinning” effect near certain price levels where there is substantial open interest. To maintain a neutral position, market makers dynamically buy or sell the underlying asset in response to price movements of options, reinforcing the pinning effect. This equilibrium, however, can be shattered by unexpected events or shifts in sentiment, causing market makers to rapidly re-hedge. This leads to a sudden and significant price and volatility movement, reflecting the delicate and interconnected nature of options trading, market making and asset dynamics. This is precisely what occurred.

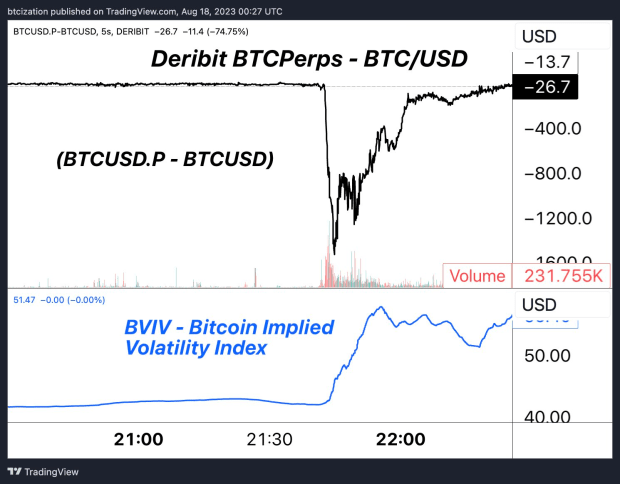

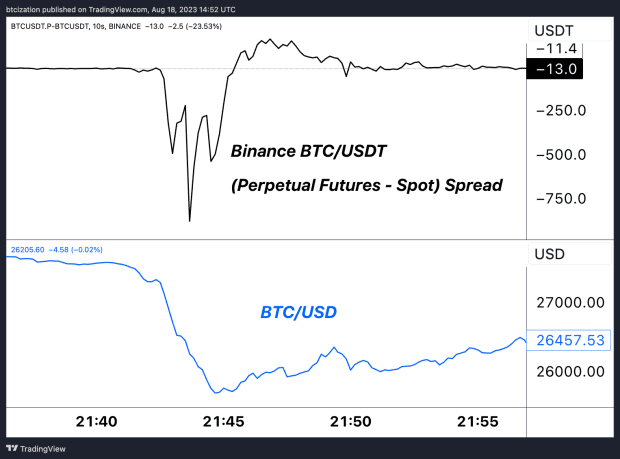

Looking at Deribit, the primary options marketplace for bitcoin/crypto, the spread between their perpetual swaps market and the spot bitcoin market widened massively as implied volatility expanded. Participants who had been making money by shorting or selling volatility were caught unexpectedly, leading to a massive dislocation and liquidation event.

As implied volatility expanded, the spread between perpetual swaps market and spot bitcoin widened on Deribit.

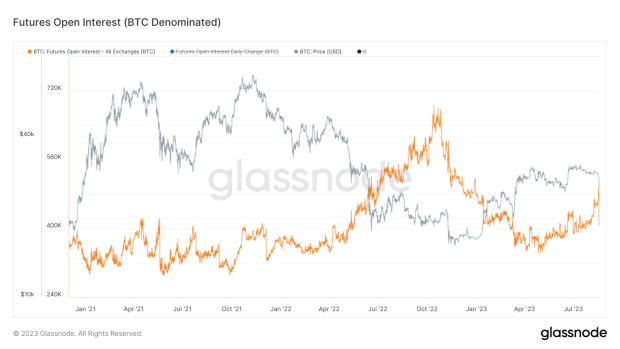

All that being said, this wasn’t just an options-driven event. There was growing leverage in the futures market as well. Spot market volumes at multi-year lows combined with growing derivative volumes and open interest in addition to volatility near multi-year lows, was akin to lighting a match near a pile of dynamite and waiting for ignition. Alas, a spark was lit.

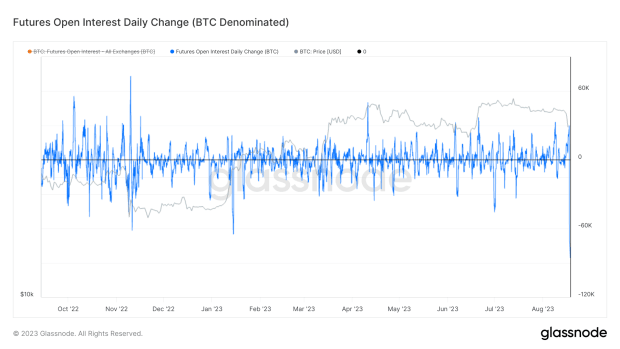

In bitcoin-denominated terms, the daily change in open interest was larger than the collapse of FTX, with 89,000 BTC less open interest than 24 hours prior.

After the move, there was 89,000 bitcoin less open interest than 24 hours prior.

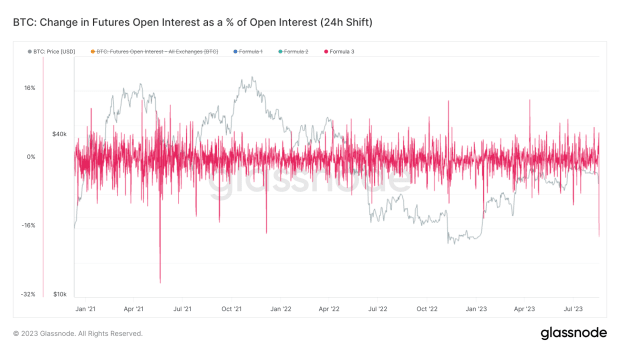

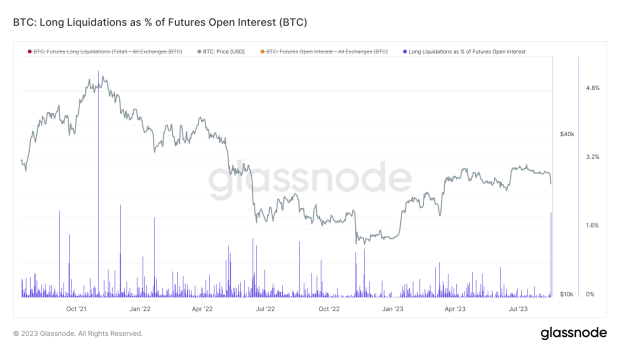

As a percentage of the futures market, with a 24-hour period to match up the timelines, the move was equivalent to 18% getting wiped out or closing, something that hasn’t been seen since December 2021.

The clearing of 18% of open interest hasn’t been seen since December 2021.A build up of open interest led to a clearing event on Thursday.A build up of open interest led to a clearing event on Thursday.

Looking only at open interest liquidations, Glassnode finds 8,141 BTC getting liquidated during Thursday’s move, the largest since November 2021, and approximately 2% of open interest that forcefully got liquidated or margin called.

8,141 bitcoin were liquidated during Thursday’s move.Long liquidations spiked during the price correction.

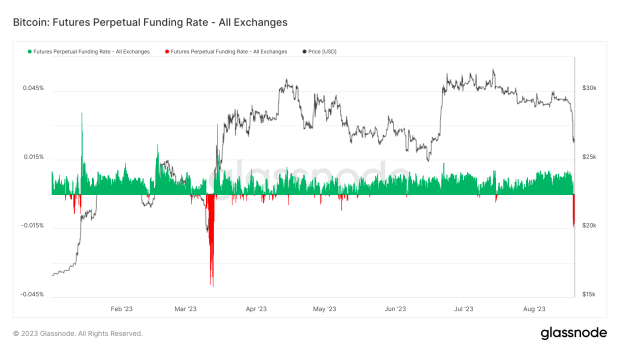

Taking a look at funding rates — the variable interest rate paid between long and short positions in the perpetual futures market to incentivize traders to keep the contract price close to the spot market — funding fell to its lowest level since the March banking crisis when Silicon Valley Bank failed and USDC depegged. This shows just how large the dislocation in the derivatives market was relative to the spot market. While it’s too early to draw conclusions about a significant short bias in the market due to the negative funding rate, we will monitor the market over the coming days and weeks. A period of sustained negative funding with rising open interest could bring about conditions conducive to a short squeeze, although this has yet to develop.

A period of sustained negative funding with rising open interest could bring about conditions conducive to a short squeeze.On Binance, the spread between perpetual swaps market and spot bitcoin widened as the price crashed.

Final Note:

In conclusion, while Thursday’s move was the largest bout of volatility seen all year and the largest bitcoin derivative-driven phenomenon in quite some time, it is typical of periods of extremely low realized and implied volatility in any market, let alone that of a notoriously volatile and unpredictable digital asset still in its monetization phase. In the short term, we now expect a pickup in volatility and greater uncertainty as the price tries to find a new equilibrium point, with plenty of news ahead regarding potential bitcoin spot ETF approvals heading into 2024.

That concludes the excerpt from a recent edition of Bitcoin Magazine PRO. Subscribe now to receive PRO articles directly in your inbox.

A space for discussion became a source of employment, creativity and fun, with Bitcoin Twitter offering a new perspective on money.Watch This Episode On YouTubeListen To This Episode:BitcoinTVAppleSpotifyGoogleLibsynOvercastRumbleMusic is a wonderful thing. Bitcoin, too, is a wonderful thing. Combine them and you have a simply fascinating mixture. One of my favorite people to work with…

Even though burglars managed to steal the victim’s hardware wallet, his funds were still safe because of his multisig setup.Bitcoin user Callum McArthur’s house was broken into last month, and the burglars stole his hardware wallet and recovery words which stored his bitcoin stack. However, even though the criminals managed to get away with McArthur’s…

Bitcoin Magazine Bitcoin Price Set for Big Move as Volatility Drops Bitcoin appears to be on the verge of a major price movement, and data suggests that volatility could return in a big way. With Bitcoin’s price action stagnating over the past few weeks, let’s analyze the key indicators to understand the potential scale and

The People's Bank of China (PBoC), China's central bank, has its eyes on cryptocurrency companies that run airdrop campaigns in the country. In its most recent financial stability report for 2018, which was published on Friday, November 3, 2018, the bank said there has been a surge in the number of "disguised" Initial Coin Offerings…

Bitcoin has surged past the $50,000 mark today, according to CoinMarketCap data, reaching this milestone for the first time since December 2021. CoinMarketCap The breakthrough marks a significant recovery for Bitcoin, which faced massive volatility and fluctuations over the last couple years, reaching lows of around $16,000. Bitcoin's resilience and upward trajectory underscore its status as a

Enhancing Creditworthiness with Bitcoin in a Debt-Intensive Economy Since US President Richard Nixon announced in 1971 that the US dollar would no longer be convertible into gold at a fixed rate, central banks around the world have started operating a fiat-based monetary system with floating exchange rates and no currency standard. As a result, the

Bitcoin can serve as an excellent gift for those trying to introduce people to the technology who may not have taken the plunge on their own.This is an opinion editorial by Koa Frederick, Senior Vice President of SaaS strategy at Accelerate Agency.Giving gifts can be a tricky thing. Plain old cash seems low effort. Socks…

Bear market woes continue for miners as bitcoin’s price sits 70% off its record highs. But hope springs eternal.Public mining companies are entering the final quarter of 2022 battered and bruised after nine months of bear market brutality. At the end of Q3, the total market values of all U.S.-listed mining companies dropped by over…

Mainstream bitcoin exchanges which collect troves of user data have warped users’ expectations for privacy-preserving, peer-to-peer versions.This is an opinion editorial by Okada, mechanical engineer and contributor to peer-to-peer bitcoin exchange RoboSats.Buying your first bitcoin has dramatically changed since the early days of trading on forums or Internet Relay Chat (IRC). Large exchanges sprung up…